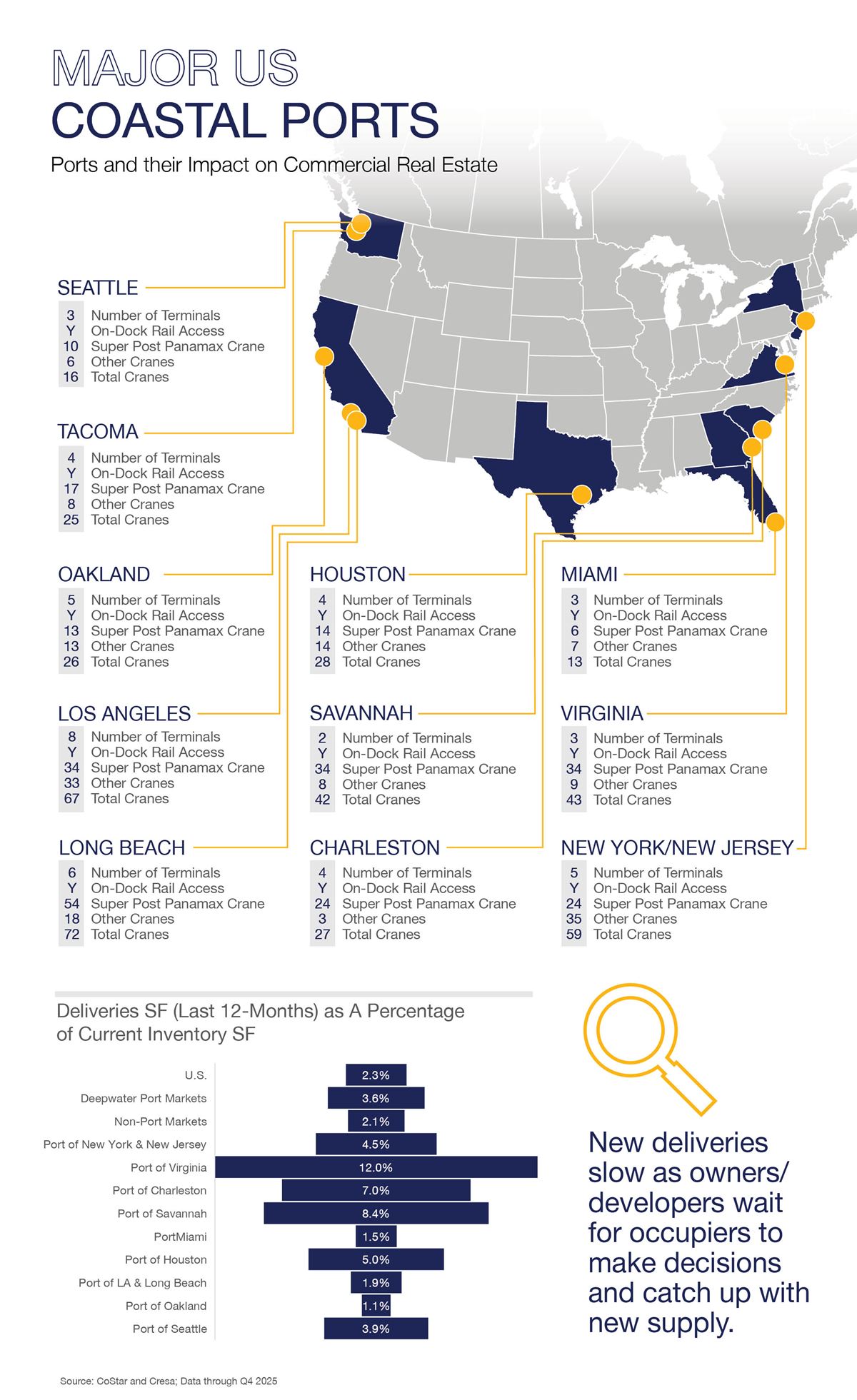

U.S. Ports Report

The health of American sea ports is generally stable but uneven. Container volumes at the largest in the U.S. have normalized from the extreme volatility of the pandemic-era surge. Most major gateways have worked through the severe vessel backlogs that defined both 2021 and 2022. Significant investments in dredging, berth expansions, and rail and yard automation have improved physical capacity and resilience. Still, operational challenges exist. Labor constraints, chassis and equipment imbalances, and rail and truck bottlenecks can slow cargo velocity, despite berth availability. In addition, policy uncertainty around trade and equipment sourcing has tempered the pace of modernization at some terminals.

Consumer spending plays an outsized role in port performance due to the large share of containerized imports of retail goods, electronics, apparel, furniture, and household products. While consumer spending remains positive, it has moderated and shifted towards services over goods compared to earlier in the decade. This shift has softened import growth at several large container ports, contributing to flatter year-over-year throughput in some markets. When consumer demand accelerates ahead of peak retail season, ports typically see corresponding spikes in inbound containers. Conversely, when consumers pull back or rotate spending toward travel and experiences, container volumes ease. Overall, the largest ports in the U.S. are positioned for steady performance through the next few quarters, with upside tied to stronger goods demands and downside risk from economic softening, trade policy shifts, and geopolitical tensions.

Download the full report to read more.